An op-ed, short for “opposite the editorial page”, is a written prose piece, which expresses the opinion of an author usually not affiliated with the publication’s editorial board.

Editor’s note: Prince Albert-based economist Kaase Gbakon does a deep dive into African natural gas.

KEY TAKEAWAYS

- Equatorial Guinea and Nigeria on August 15, 2024, signed a bilateral agreement for the joint construction of the Gulf of Guinea Gas Pipeline Project to assure gas feedstock supply to Equatorial Guinea’s Gas Mega Hub (GMH).

- At the heart of the GMH is the Punta Europa Park, an integrated gas development, which includes a 3.7 MMtpa LNG and 1.1 MMtpa Methanol plant.

- As of 2018, the EG government had earned $12 billion in royalties, taxes, dividends, and bonuses from Punta Europa Park.

- However, gas supply is in imminent decline as capacity utilization at the Punta Europa Park has declined from 95% in 2018 to 45% in 2023.

INTRODUCTION

Presidents Teodoro Obiang Nguema Mbasogo of Equatorial Guinea and President Bola Ahmed Tinubu of Nigeria had on August 15, 2024, signed a bilateral agreement for the joint construction of a pipeline – called the Gulf of Guinea Gas Pipeline Project. The package which is the subject of the agreement includes:

- The joint development of a regional gas pipeline between Nigeria and EG.

- The supply of gas from Nigeria to the EG gas park which includes an LNG processing plant, power, and industrial customers.

This agreement was on the back of a memorandum of understanding (MOU) signed between Nigeria and Equatorial Guinea in early 2022. The MoU was to allow the commercialization of untapped gas reserves in the proximity of the border via an offshore gas pipeline to the EG gas park.

Previously, in March 2023, Equatorial Guinea had signed a bilateral trade agreement with Cameroon for the joint development of oil and gas fields along their shared maritime borders. The fields targeted for development in the treaty were the Yoyo and Yolanda fields, the Etinde gas field, the Camen field and the Diega field.

These coordinated treaties are meant to assure gas feedstock supply to Equatorial Guinea’s Gas Mega Hub (GMH) and elevate the country as a regional infrastructure hub.

However, what will this mean for Equatorial Guinea? And what are the enablers for such a project?

Let’s find out!

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

EQUATORIAL GUINEA’S GAS VISION

Since Equatorial Guinea’s discovery of large oil reserves in 1996, the country has seen a significant economic boom. Between 2007 and 2014, she was Africa’s richest country on a per-capita basis. The entire hydrocarbon production in Equatorial Guinea comes from offshore fields. In the case of natural gas, the whole production comes from shallow water terrain.

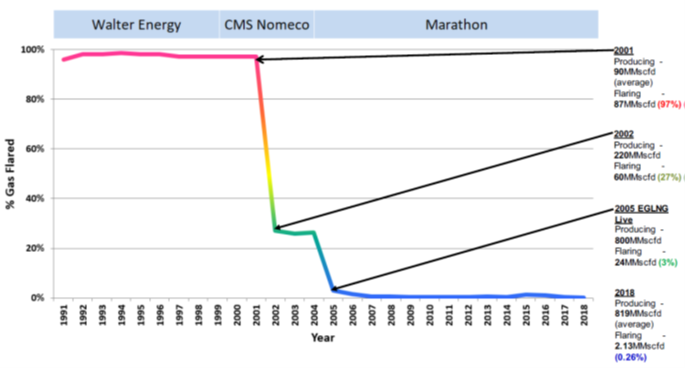

The reduction of flared gas was a primary motivation which drove the EG government to embark on the construction of the “gas industrial park” which took place over a period of nine (9) years, from 1997 to 2006. Between 1991 and 2001, ~100% of natural gas was flared, which had reduced to 27% by 2002 with the commencement of the Methanol plant. As of 2018, barely 3% of the natural gas produced in EG was flared. See Figure 1.

Fig. 1: Trend of Percentage of Gas Flared in EG (Source: Marathon)

Gas to the Punta Europa Park had been supplied solely from the Marathon Oil EG-operated Alba Field and starting in 2021 supply was supplemented by gas from the Noble-operated Alen field. The Alba gas field, with its 3 Tcf reserves was sufficient to cater to only 12.5 years of the 17-year LNG offtake agreement with BG.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

PUNTA EUROPA, THE GAS MEGA HUB

Equatorial Guinea signed agreements with Marathon Oil, Noble Energy, Atlas Petroleum, Glencore and Gunvor to process stranded gas from the Alen and Aseng gas fields in 2019. This launched Africa’s first offshore Gas Mega Hub (GMH).

At the heart of Equatorial Guinea’s GMH is the Punta Europa Park located on Bioko Island, offshore Malabo. The facilities of the Punta Europa Park include:

- a 3.7 MMtpa LNG plant,

- 1Bcf/d Gas treatment plant with condensate handling and storage facilities,

- 1 MMtpa Methanol plant

- Two (2) gas power plants with combined capacity of 27 MW and

- Two (2) world class berthing facilities for LPG and LNG export vessels among others.

These gas utilization projects concentrated in the park together utilize circa 780 MMscfd.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

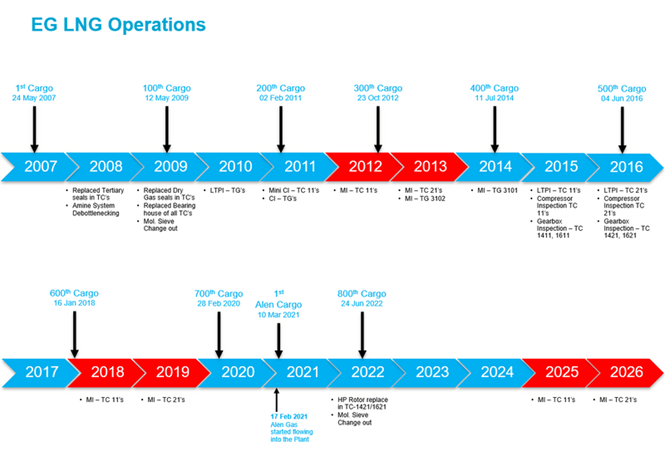

Development Timeline

The timeline for the development of the Punta Europa goes back to 1984 with the drilling of discovery well. Key milestone dates have been highlighted below:

- 1984: Discovery well GEPSA 13B1-1X drilled

- 1991: Initial production by Walter International commenced.

- 1998: Construction of the Methanol plant begins.

- 1999: Operations of the 10MW power plant commence (Construction started 1997)

- 2001: operations of the Methanol plant commence.

- 2002: The 17MW power plant commences operation (Construction started 2000)

- 2004: The EGLNG FID is sanctioned.

- 2007: First production from the EGLNG in 2007.

The time from FID in 2004 to first cargo in 2007 made EG LNG one of the world’s fastest LNG projects from FID to first cargo.

Figure 2 below shows milestones in the operations of the EG LNG

Fig. 2: Milestone illustration of the EG LNG Operations (Source: EGLNG)

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

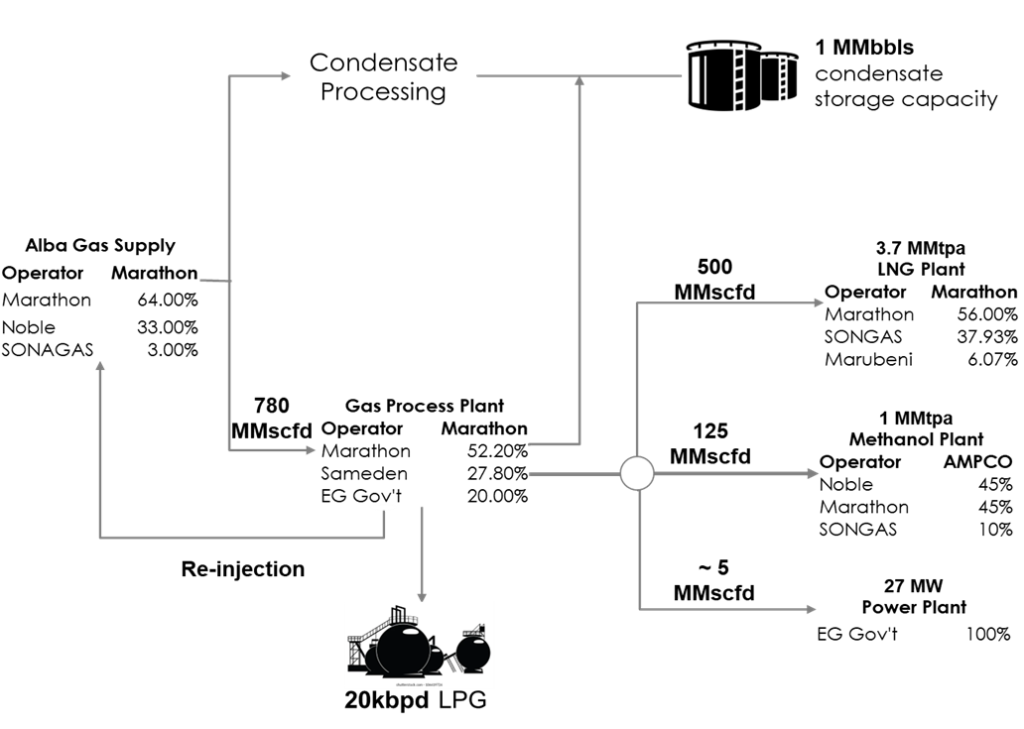

Ownership Structure

In 2002, Marathon Oil Corporation acquired CMS Energy’s stake in the Alba fields and set off the plan to monetize the field’s gas through LNG exports. Marathon Oil, through its wholly owned subsidiaries, is the operator and majority shareholder of the integrated gas business at Punta Europa.

Marathon owns a 64% operated working interest in the upstream Alba Unit, 52% interest in the Alba Plant LLC, which operates the onshore LPG processing plant, 56% of EGHoldings, which operates the 3.7 MMtpa LNG production facility, and 45% of the Atlantic Methanol Production Company (AMPCO), which operates the 1 MMtpa methanol plant.

Figure 3 captures the ownership structure and gas flow schematic across the value chain in the park.

Fig. 3: Ownership structure and gas flow schematic

Other participants across the park include:

- Sociedad Nacional de Gas de Guinea Ecuatorial (SONAGAS), the Equatorial Guinean national natural gas company formed in 2005.

- Noble Energy E.G. Ltd, a Chevron company.

- Marubeni Corporation, one of Japan’s largest general trading and investment companies with interests in 3 other LNG Projects: Qatar, Peru and Papua New Guinea.

- Samedan of North Africa, LLC a wholly owned subsidiary of Noble Energy

According to a report from Marathon, as of 2018, the government of Equatorial Guinea had earned a total $12 billion from a combination of royalties, taxes, dividends, and bonuses from across the Punta Europa value chain.

By 2022, 64 MMtpa of LNG had been produced and lifted from the park. However, the party is facing a near end – if nothing is done about the gas supply.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

EQUATORIAL GUINEA: GASSED OUT

It has always been known that production from the Alba field will face imminent decline and will result in massive, unsustainable deficits if not quickly backfilled. That was why in 2019, Equatorial Guinea kicked off its endeavour to become Africa’s premier gas hub – a project known as the Gas Mega Hub.

This agreement resulted in the commencement of supply from the nearby Noble-operated Alen field in February of 2021. The Alen field development features a 70-km, 24-inch pipeline tied back from the Alen field to the onshore Alba gas processing plant. Designed to convey 950 MMscfd of gas, the project cost $330 million to develop.

Despite this development, the field has only 0.6 Tcf, which will be unable to sustain the LNG Plant capacity beyond 5-6 years.

Evidence of Decline: Exhibit A

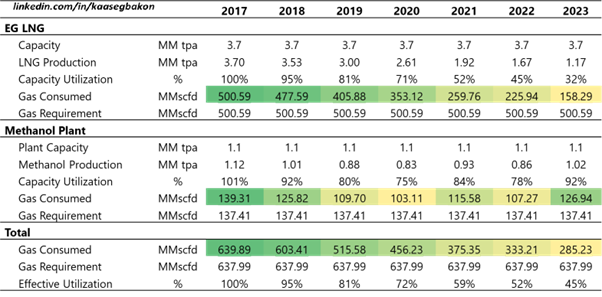

The declining trend in LNG and methanol production occasioned by the declining gas supply has been evident since at least 2017.

Table 1: LNG and Methanol Production Trend from Punta Europa

For the LNG plant, the gas supplied to the plant declined precipitously by 68% from 500.59 MMscfd in 2017 to 158.29 MMscfd in 2023. As of 2023, the LNG plant was operating at only 32% of its full capacity.

Gas consumed for Methanol production also declined from 139.31 MMscfd in 2017 to a low of 103.11 MMscfd in 2020, and then an upward swing to 126.94 MMscfd in 2023. Overall a 9% decline from the 2017 gas consumption level.

In total, the gas consumed by the Punta Europa Park is only 45% of the full capacity as of 2023 down from 95% utilization rate in 2018. Clearly there is more room to improve the revenue inflows to the Punta Europa Park.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

Evidence of Decline: Exhibit B

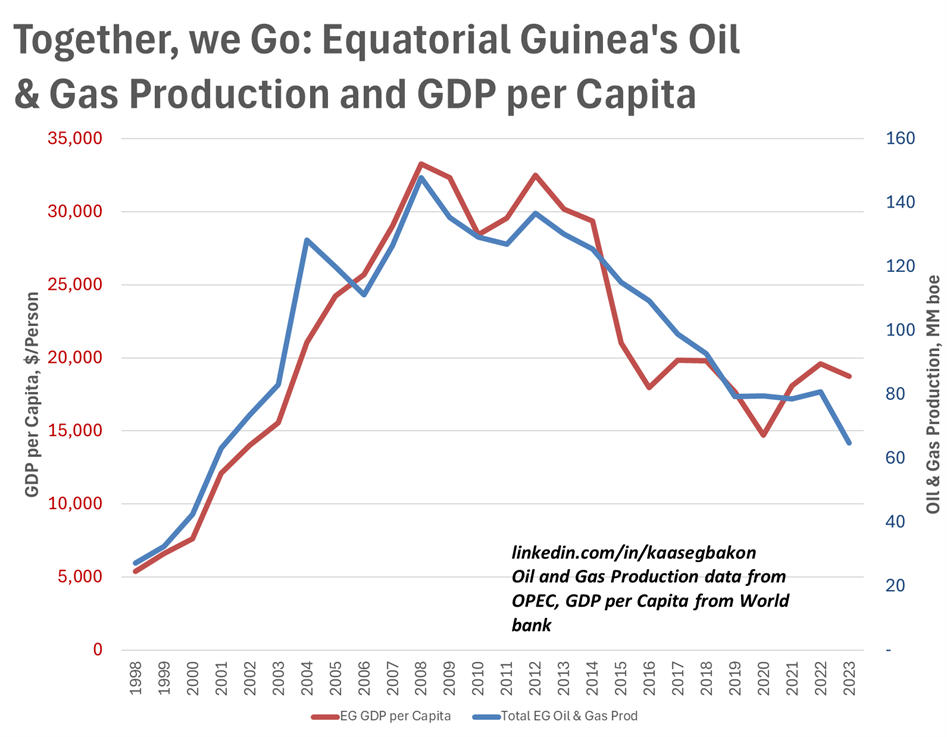

In 2022, oil and gas accounted for more than 70% of the EG’s government revenues and nearly 50% of both exports and gross domestic product (GDP).

It is no surprise then, that the decline in oil and gas production has also been accompanied by a decline in GDP per capita as noted in Figure 4. EG’s GDP per capita peaked at $33,270/person in 2008 when circa 150 MMboe of oil and gas was produced. As of 2023, with oil and gas production down to 65 MMboe, the GDP per capita had declined to $18,732/person.

Figure 4: Equatorial Guinea’s GDP per capita [PPP (current international $)] and Oil and Gas Production

The GDP per capita has declined at a rate of 3.76% per annum from its 2008 peak to its 2023 level. This highlights the case for improved gas supply to the GMH.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

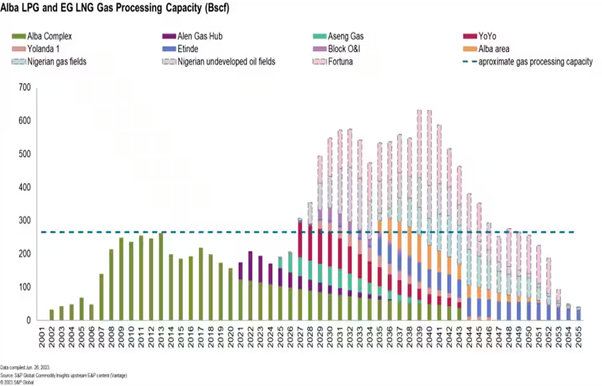

Where will Gas Come From?

The map in Figure 5 shows the nearby fields surrounding Equatorial Guinea targeted for gas supply. These fields lie within the territorial zones of Nigeria and Cameroon. The thrust behind the GMH is to make Punta Europa the choice destination for monetization of the regional gas resources.

Fig. 5: Map Showing the Gas Resource Opportunities Around Equatorial Guinea (Source: Marathon)

The potential gas supply sources proximate (within tie back distance) to the gas hub, hold total reserves estimated to be at least 6 Tcf, which can last 20 years given that the gas requirement of the EG LNG and other facilities in the park is ~ 285 Bcf/yr (780MMscfd).

Fig. 6: Forecast Gas Production from Fields close to Punta Europa Park (Source: S&P)

Of the total reserves from proximate sources of 6 Tcf, Nigeria holds about 3 Tcf. This is why the Gulf of Guinea pipeline project holds the key to the badly needed lease of life for the hub while also creating monetization opportunity for Nigeria.

So, what will it take to supply? A pipeline must be built of course. Let’s see how!

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

PIPELINE TO BIOKU: THE INGREDIENTS OF GAS SUPPLY

The proposed pipeline in the bilateral agreement with Nigeria is a transnational infrastructure. Let us have a look at what is required for such a project within the context of Equatorial Guinea’s GMH as well as the economics of gas supply to the hub.

- Funding arrangement and ownership structure for pipeline: The title of the bilateral agreement has given this away. We can assume the pipeline will be jointly developed, with the ownership structure reflecting the joint effort. The cost of development also needs to be delineated. However, the specifics are not clear.

- Fiscal System for the Transnational pipeline: Given that the pipeline with run between two sovereign countries, both nations will have to agree and ratify the applicable fiscal system. The fiscal system addresses issues of how the infrastructure will be taxed, the proportion for sharing tax receipts, categorization and treatment of expenses, and the mechanisms for dispute resolutions. We have the West African Gas Pipeline (WAGP) to look to as an example.

- Upstream Gas development: Alongside the arrangements to develop the pipeline, upstream gas field development plan will be required. There are factors that drive this requirement such as the attribute of candidate fields (resource size, resource type, distance to Punta Europa), applicable fiscal regime, cost of development.

- Supportive Gas pricing framework: the price of gas delivered to the park has to be low enough to enable the GMH to develop profitably, while at a sufficient level to ensure the economic viability of the development upstream gas supply. Inclusive in the pricing of the gas to the park will be the pipeline tariff. Gas has been supplied to the Punta Europa Park at $0.24/Mscf from the Alba field, while the price of the produced LNG was indexed to Henry Hub under the recently lapsed offtake agreement with BG.

- Alignment of Strategic Interests: While the EG government requires gas from Nigeria and Cameroon to fulfil its vision of creating a GMH, these countries may also have plans for these resources. To progress project development, strong inter-regional cooperation is required with EG providing a strong case to its neighbours as to why its GMH is the pathway to rapid monetization of these resources.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

THE GULF OF GUINEA GAS PIPELINE TARIFF

A critical component of the assessment of economic viability of the GMH is the price at which to supply the gas feedstock, which will include the pipeline tariff. In this note, we will focus on modeling the pipeline tariff – after all, the bilateral agreement was for the joint construction of a pipeline.

Our key assumptions are:

- The Oron 2 field is gas source from Nigeria as seen from this report from the @AdvisorsReport located 110km to the EGLNG.

- The pipeline is sized to transport 1 Bcfd of gas.

- The applicable fiscal system is that for midstream facilities in Nigeria.

Table 2 shows Project cost assumptions.

Table 2: Gulf of Guinea Pipeline Cost Assumption

We model pipeline economics on the assumption of $545 million CapEx and fixed OpEx at 5% of CapEx per annum.

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

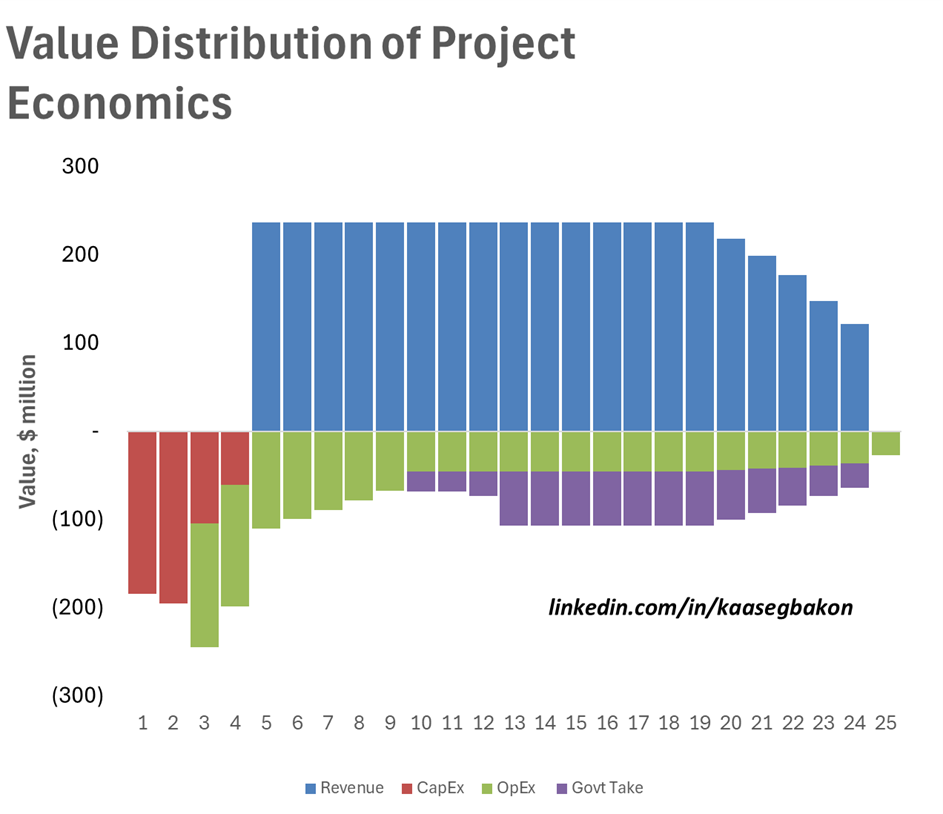

Results

The model suggests that a pipeline tariff of $0.65/Mscf is required for the project to return a 12% Internal Rate of Return (IRR). At this tariff level, a total revenue of $4,423 million is realized by the project, of which total tax payments to government amount to $741 million. Figure 7 shows the value distribution from the project over time.

Figure 7: Value distribution of Gulf Guinea Pipeline Economics

The biggest driver of the tariff is the pipeline CapEx, remember however that the tariff is only one component of the price of gas delivered to the Punta Europa Park.

Value chain economics of the project will be required to evaluate all stakeholders’ benefit from the inter-regional cooperation to deliver the GMH.

WHAT NEXT FROM HERE

It should be clear that the development of the GMH and economic well-being hinges on the life line gas supply from regional players – Nigeria and Cameroon. The signing of MoUs and treaties is one thing, rapid project development to get gas to market is another.

The GMH can play a significant role in monetizing gas supply from Nigeria and Cameroon, establishing a foothold in the LNG market, retaining the interest of investors in the region, and providing much needed revenue, economic growth and energy security for the 1.7 million people of Equatorial Guinea.

The clock is ticking!

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001