David Yager is a long-time oilpatch writer and executive. Yager’s copy is provided free of charge by the Canadian Energy Centre Ltd.

Thirty years ago, I had the opportunity to meet the secretary general of OPEC, Dr. Subroto of Indonesia. He was visiting Calgary and being squired about by Alberta Energy Minister Rick Orman. We met at the Lake Louise ski hill at the end day.

But the liquid my brain was thinking about was beer, not petroleum.

Although we get along well today, in 1991 Minister Orman was not the head of my fan club. We were engaged in a very public media disagreement over Alberta’s oil and gas royalty rates. Despite years of tough times, they had not been reduced from the high price era of the late 1970s and early 1980s.

I had no personal quarrel with Minister Orman. I was just doing my job as an oil writer in pushing the province to leave enough cash flow in the industry to keep the lights on for the oil services sector.

Walking back to the bar after putting my gear in my car, I ran into Minister Orman, who suggested I introduce myself to Dr. Subroto whom he pointed out was standing close to the lodge waiting for his ride back to Calgary.

This was more of a challenge than an opportunity. I couldn’t say no. It wasn’t hard to identify the only Indonesian wearing ski clothing.

But what to do you say to the secretary general of OPEC after oil prices have been in the dumpster and the industry on its knees for years?

The obvious. “Honoured to meet you, Dr. Subroto. What is going to happen with oil prices?”

Is there anyone in the world more qualified to answer?

He replied, “The only thing certain about oil is uncertainty.”

Take that to your banker, investors or board of directors.

The events of the last few weeks remind us, yet again, that Dr. Subroto was right. From WTI’s recent peak of US$85.64 on Oct. 25, North America light sweet crude dropped 20 per cent by Nov. 26 to close at US$68.17. Half that drop took place in a single day.

Oil has been softening for weeks due to a series of events that nobody in business, commodity trading or financial markets could have predicted; another unwanted and unforeseen flock of black swans.

- 0132 UMWA 20260132 UMWA 2026

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

A year ago, Democrat Joe Biden won the American presidential election on a platform targeting North America’s oil and gas industry. This included cancelling the Keystone XL pipeline, ending leases sales on federal lands, tax changes to make investing in new production less attractive, renewed methane emission reduction targets and hundreds of billions in funding and subsidies for low carbon energy and electric vehicles.

Oil prices have been rising based on factors everyone understands; understandable and predictable market fundamentals like supply, demand and public capital markets pressing publicly traded oil companies for higher dividends, not higher oil production.

As oil prices rise, so do U.S. gasoline prices. Consumers don’t like that, and never have. Voters are schizophrenic about oil. They support politicians who claim we must use less to save the world, but they don’t understand that achieving this requires them to use less, pay more or both.

Curveball number one came completely out of left field last August, when President Biden called on OPEC+ to increase oil production to reduce pump prices. At this time WTI was US$70 a barrel.

American oil producers shook their heads in disbelief and OPEC+ politely responded that they had no intention of adjusting their existing production increase schedule to help Biden politically.

Following Biden’s first act as president to cancel the Keystone XL oil pipeline from Canada, it was not intuitive that only seven months later he would be calling for more oil from Russia and the Middle East.

At the G20 meeting in Rome in late October that preceded the COP26 climate conference in Glasgow, Biden raised the issue again. He asked every country that could produce more oil to do so, and again mentioned OPEC+.

He then went to the COP26 and agreed with everyone that climate change was an enormous challenge, and the United States would join all other countries in committing to do more to use less fossil fuels.

After the 2022 mid-term elections of course.

Back home, curveball number two appeared when Biden started musing about using oil from America’s Strategic Petroleum Reserve (SPR) to dampen prices. He managed to persuade other countries like China, South Korea and Japan to do the same, or at least say they would.

The SPR is supposed to deal with a shortage of oil, not a shortage of votes for the Democrats. The official announcement took place Nov. 23. By this time, Biden had talked and postured about US$9 a barrel off of WTI’s October peak.

Meanwhile, OPEC+ looked at its outlook for the rest of 2021 and early 2022 and determined that its latest forecast for demand growth could be optimistic if all the countries do what they say with their oil reserves. OPEC+ is set to meet again Dec. 2, and has said it may adjust output to offset these new supplies and maintain price stability.

Curveball number three came with the announcement of a new COVID virus identified in South Africa that the World Health Organization declared a “variant of concern.” It was even given a name – Omicron.

Governments around the world immediately banned incoming flights from southern Africa. This would obviously affect the slowly recovering global jet fuel market.

Combined with the U.S. Thanksgiving holiday Nov. 25, on Nov. 26, crude tanked, losing US$10 in a single day. As oil traders ate turkey, they appear to have left the market to trading algorithms.

- 0132 UMWA 20260132 UMWA 2026

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

The same week the Canadian Association of Energy Contractors released it 2022 drilling forecast which showed a 25 per cent increase for next year. Assuming it can find enough skilled workers to operate the equipment.

Two weeks earlier, the Petroleum Services Association of Canada put out its 2022 drilling forecast showing 16 per cent more wells. It, too, talked about the challenges of attracting workers back to the oilpatch after laying off so many only 18 months ago.

What can we expect?

Outside of the headlines and the significant gyrations in the values of publicly traded oil and gas stocks, this oil market turmoil will have no material impact on activity and spending next year.

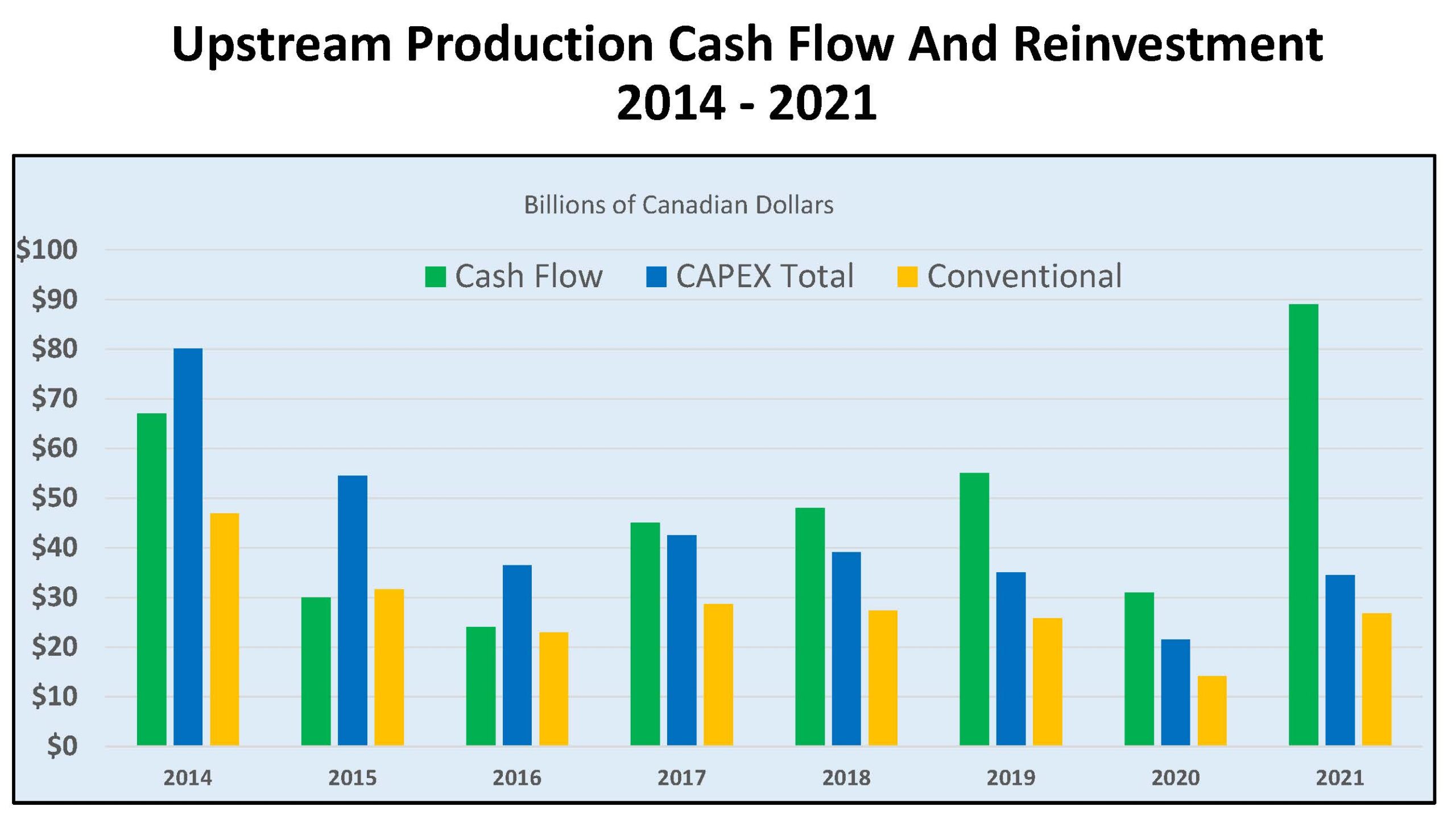

ARC Energy Research Institute publishes a weekly macroeconomic overview of Canada’s upstream oil and gas industry. The Nov. 22 version shows how healthy the industry is compared to prior years and current volatile oil markets (note – 2020 and 2021 are flagged as estimates).

Source: ARC Energy Research Institute. 2020 and 2021 are flagged as estimates.

The 2021 financial recovery has been spectacular. Combined oil and gas production will reach a record 8.2 million barrels of oil equivalent per day at the highest average prices since 2014. Total revenue from production this year could be $159 billion, exceeding the last high-water mark of $145 billion in 2014 by a wide margin.

The important number for the working oilpatch is cash flow from production – how much money is available for reinvestment after paying all operating costs, taxes and royalties. After reaching $67 billion in 2014, it has stayed well below that level since. In 2020 it was only $32 billion, less than half of the 2014 peak.

This year ARC is predicting record cash flow due in part to the operating efficiency of the industry after six years of tough times. The estimate for 2021 is $89 billion, one-third higher than the previous record.

Despite having more cash than ever for capital investment, the industry is being very cautious. Estimated CAPEX for 2021 is only $35 billion, $27 billion for conventional production and $8 billion for oil sands.

Producers have been paying down debt and spending on catch-up maintenance. They are understandably cautious after all the pressure the ESG investment movement has put their key financial providers – equity, debt and even insurance.

But the good news is that even if the current WTI price does not recover, there’s still lots of internally generated cash flow available for the modest (compared to prior years) spending increases predicted for 2022.

The unforeseen events that have caused oil to lose 20 per cent of its value in the past month will not affect current spending plans unless things get much worse.

Which is unlikely given global market fundamentals. And, hopefully, no more black swans.

- 0132 UMWA 20260132 UMWA 2026

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001

Then came curveball number four. Along with Washington’s decision to manage the price by releasing oil from the SPR, the government also asked American producers to increase oil production. In the United States this can only be done by drilling.

On Nov. 23 Reuters reported that U.S. Energy Secretary Jennifer Granholm “… urged U.S. energy companies to increase oil supply amid ‘enormous profits’ as President Joe Biden seeks to bring down the price of gasoline for American families. Granholm said the oil and gas industry had leases on 23 million acres of public lands on and offshore and thousands of permits that were not being used.”

Not apparent to the energy secretary is that U.S. producers are not withholding production but have stopped aggressive drilling in the major light tight oil basins. Which is what both the federal government and capital markets have been telling them to do for the past year.

That many Democrats don’t know how the U.S. energy industry functions was revealed again by New York Congress representative Alexandria Ocasio-Cortez, who gained notoriety for her aggressive support of the Green New Deal to replace fossil fuels.

In a video clip widely circulated on social media, AOC said she didn’t support Keystone XL or the Enbridge Line 3 expansion because the United States had no need for new pipelines to export natural gas.

She was blissfully unaware that both were intended to carry imported oil.

Feel free to be confused by curveball number five. After fulfilling an election pledge to stop issuing new drilling permits on federal lands, the U.S. government was taken to court and lost. So on Nov. 18, Washington approved the leasing of up 1.7 million acres of 80 million acres opened for bidding in the Gulf of Mexico. The federal government received proceeds of US$192 million, with Chevron and ExxonMobil being the top two buyers.

Three decades after Dr. Subroto warned me that oil markets will always be uncertain, the events of the last few months have proven he was correct then and remains correct now.

Fortunately, what lurks behind all these non-predictable events are supply, demand and consumer choice.

This last bout of market gyrations should end soon. Oil is much more likely to see US$100 a barrel before it again sees US$30.

But nowadays, oil prices will never truly be certain.

David Yager is an oil service executive, oil writer and energy policy commentators and analyst. He is currently President and CEO of Winterhawk Casing Expansion Services which is commercializing a new way of mitigating methane emissions from surface casing vent flows. He is author of From Miracle to Menace – Alberta, A Carbon Story. More at www.miracletomenace.ca.

- 0132 UMWA 20260132 UMWA 2026

- 0131 SASPO-2874_Self Serve Campaig0131 SASPO-2874_Self Serve Campaig

- 0130 SKTL_Starlink_Ranch_16x9_Clean0130 SKTL_Starlink_Ranch_16x9_Clean

- 0129 Turnbull drivers operators0129 Turnbull drivers operators

- 0128 OSY Rentals updated0128 OSY Rentals updated

- 0126 Steel_Reef_Promo_0126 Steel_Reef_Promo_

- 0125 SASPO-2896_Right of Way_Awareness_20250125 SASPO-2896_Right of Way_Awareness_2025

- 0118 IBEW 30 sec0118 IBEW 30 sec

- 0114 Prospera Bold Vision0114 Prospera Bold Vision

- 0113 Miller Epic Cinematic Hollywood trailer0113 Miller Epic Cinematic Hollywood trailer

- 0102 Lori Carr Coal Extended0102 Lori Carr Coal Extended

- 0099 Mryglod Steel 1080p0099 Mryglod Steel 1080p

- 0095 Fast Trucking nearly 70 years good at it0095 Fast Trucking nearly 70 years good at it

- 0046 City of Estevan This is Estevan Teaser0046 City of Estevan This is Estevan Teaser

- 0077 Caprice Resources Stand Up For Free Speech0077 Caprice Resources Stand Up For Free Speech

- 0061 SIMSA 2024 For Sask Buy Sask0061 SIMSA 2024 For Sask Buy Sask

- 0051 JML Hiring Pumpjack assembly0051 JML Hiring Pumpjack assembly

- 0049 Scotsburn Dental soft guitar0049 Scotsburn Dental soft guitar

- 0041 DEEP Since 2018 now we are going to build0041 DEEP Since 2018 now we are going to build

- 0032 IWS Summer hiring rock trailer music

- 0022 Grimes winter hiring

- 0018 IWS Hiring Royal Summer

- 0013 Panther Drilling PO ad 03 top drive rigs

- 0002 gilliss casing services0002 gilliss casing services

- 9002 Pipeline Online 30 sec EBEX9002 Pipeline Online 30 sec EBEX

- 9001